Whether criminal prosecution for cheating will continue after settlement of loan by way of compromise in DRT?

2. A short but interesting question which arises for consideration in this appeal is whether a criminal prosecution can be initiated under Sections 420 and 471 of the Indian Penal Code, 1860 and allowed to continue after settlement of the loan account by way of an approved compromise and which had the imprimatur of the Debts Recovery Tribunal?

3. The above question arises in the context of a challenge by the appellants to the order dated 05.07.2024 passed by the High Court of Chhattisgarh (‘High Court’) in Cr.M.P. No. 1361 of 2023 (Vijay Kumar Kela & Anr. Vs. CBI & Anr.).

Prefatory facts

4. For proper adjudication of the question framed, it would be appropriate to briefly narrate the relevant facts.

4.1. Appellant No. 2 was established as a proprietary trading concern in the year 1998 dealing in agricultural inputs like fertilizers and other allied products. Elder brother of appellant No. 1 late Parmanand Kela had established appellant No. 2 firm and was managing the affairs of the said firm. Following the death of late Parmanand Kela, appellant No. 1 became the sole proprietor of the firm.

4.2. Erstwhile proprietor Parmanand Kela had applied to the UCO Bank on 28.07.2006 for extending cash credit facility of fund based limit to the extent of Rs. 50 Lakhs and non-fund based limit i.e. letter of credit to the extent of Rs. 1 crore in the name of appellant No. 2. After examining the proposal and on due consideration, cash credit facility of fund based limit to the extent of Rs. 50 lakhs and non-fund based limit i.e. letter of credit to the extent of Rs. 1 crore was extended by the UCO Bank to appellant No. 2 on 02.09.2006 on proper security, both primary and collateral. Subsequently, on application by the appellants, the credit facility was enhanced to Rs. 5 crores for which additional property was given by way of mortgage. Finally, on 30.01.2009, credit facility was extended to Rs. 8 crores (Rs. 3 crores for cash credit and Rs. 5 crores for letter of credit limit) for which the mortgaged properties were substituted by another property having higher valuation.

4.3. Parmanand Kela passed away on 28.11.2009. At that stage, appellant No. 1 stepped into the shoes of his late brother and started looking after the affairs of appellant No. 2. Appellant No. 1 informed the UCO Bank that the firm was unable to procure big orders as a result of which it was facing financial crunch. Because of financial constraints, repayment of loan amounts became irregular, following which the loan account of the appellant No. 2 was declared as a Non-Performing Asset (NPA).

4.4. UCO Bank invoked provisions of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (‘SARFAESI Act’, hereinafter) against the appellants and issued notice dated 05.02.2011 under Section 13(2) of the SARFAESI Act to the appellants.

4.5. At that stage, a compromise proposal was worked out between the two parties on 14.03.2015 which was recommended by the UCO Bank, Raipur Main Branch for sanctioning by the competent authority of the said Bank. Vide letter dated 30.03.2015, the competent authority informed the UCO Bank, Raipur Main Branch that the compromise proposal was approved and in this connection, a sanction letter was also issued for doing the needful. The settlement amount was Rs. 4.25 crores against the outstanding dues of Rs. 6.49 crores as on 14.03.2015, which included notional interest of Rs. 3.09 crores.

5. It may be mentioned that UCO Bank had filed Original Application No. 355/2011 before the Debts Recovery Tribunal at Jabalpur (DRT) for realization of the loan amount from the appellants with interest etc. In the said proceedings, a joint application was filed by the UCO Bank and the appellants for recording compromise. Vide the order dated 10.07.2015, DRT recorded the details of the compromise reached between the parties and fixed 07.10.2015 for submitting compliance with regard to the compromise settlement.

5.1. Following the same, appellants paid the settlement amount to the UCO Bank pursuant to which the latter issued no dues certificate dated 30.09.2015 certifying that the cash credit account of appellant No. 2 was settled pursuant to a compromise and that payment was received in terms of the approved compromise.

5.2. By order dated 27.10.2015, DRT dismissed OA No. 355/2011 as withdrawn in view of the fact that the entire compromise amount had been deposited by the appellants which was acknowledged in the application dated 27.10.2015 filed by the UCO bank before the DRT.

UCO Bank Zonal head registered FIR with the CBI that the appellants had got released two valuable properties mortgaged and substituted with an encroached property

6. After more than 2 years, on 27.02.2018, the Zonal Head of UCO Bank, Raipur Zonal Office submitted a written complaint to the Superintendent of Police, Central Bureau of Investigation (CBI), New Delhi stating that appellants, more particularly appellant No. 1, in collusion with certain officials of the Bank had defrauded the UCO Bank by diverting the funds of the Bank made available to the appellant firm to the account of appellant No. 1. It was further alleged that by entering into the settlement, appellants had got released two valuable properties mortgaged with the UCO Bank and substituted the above properties with an encroached property. It was submitted that the borrowers with the dishonest intention of causing wrongful loss to the Bank and wrongful gain to themselves fraudulently committed the act of cheating and thus committed offences of cheating, criminal breach of trust etc. under the Indian Penal Code, 1860 (IPC). The Superintendent of Police, CBI was requested to register an FIR, investigate the matter and thereafter to initiate appropriate criminal proceedings against the offenders.

7. On the basis of the aforesaid complaint, the first respondent i.e. CBI registered FIR bearing No. RC2202018E0002 dated 08.03.2018 under Section 120B read with Section 420 IPC and Section 13(2) read with Section 13(1)(d) of the Prevention of Corruption Act, 1988 (PC Act).

8. Thereafter, CBI filed chargesheet on 27.11.2018 before the Court of Special Judicial Magistrate, CBI Cases, Raipur (‘Special Judicial Magistrate’ for short). In the chargesheet, it is stated that investigation revealed that on the basis of forged audit reports submitted by appellant No. 1, appellant No. 2 was able to get a renewal/enhancement of cash credit limit of more than two times of the original amount sanctioned. He had forged audit reports as genuine with the intention to cheat the UCO Bank. In the process, UCO Bank suffered wrongful loss of Rs. 223.7 lakhs and unapplied interest of Rs. 308.8 lakhs and correspondingly there was wrongful gain of the said amount for appellant No. 1. Thus, he had committed the offences of cheating and using of forged documents as genuine ones which are punishable under Sections 420 and 471 IPC. It was further stated that the investigation did not disclose any proactive role played by Bank officials in respect of sanction or renewal/enhancement of the cash credit limit. Therefore, none of the Bank officials were charge sheeted. Consequently, the charges under the PC Act were dropped.

8.1. Vide order dated 20.02.2023, the learned Special Judicial Magistrate framed charges under Sections 420 and 471 IPC against appellant No. 1.

Appellants have filed quash petition

9. Appellants filed a petition under Section 482 of the Code of Criminal Procedure, 1973 (CrPC) before the High Court for quashing of the chargesheet dated 27.11.2018 as well as the order passed by the Special Judicial Magistrate dated 20.02.2023 whereby charges have been framed. The quashing petition was registered as Criminal MP No. 1361 of 2023. The said petition was contested by the respondents.

High Court dismissed the quash petition

9.1. By the impugned order dated 05.07.2024, the High Court dismissed the criminal petition prima facie observing that appellants with a fraudulent intention got released two valuable properties which were mortgaged with the Bank by substituting it with encroached property and had also enhanced the credit limit by submitting forged audit reports which was issued by the chartered accountant.

10. Assailing the aforesaid impugned order dated 05.07.2024, the instant special leave petition came to be filed by the appellants. On 13.12.2024, notice was issued.

Summation of facts

15.13. Almost after two and a half years of the DRT putting its imprimatur on the compromise vide the order dated 27.10.2015, the Zonal Head of UCO Bank, Raipur Zonal Office submitted a written complaint dated 27.02.2018 to the CBI with the request to lodge FIR against the appellants. In the written complaint, after mentioning about the compromise settlement entered into between the parties, it was stated that the UCO Bank had declared the account of appellant No. 2 as ‘fraud’ and the same was reported to RBI on 18.04.2016. It was mentioned that the element of fraud was first suspected on 20.12.2013 but the same was not discernible beyond doubt. The account was not treated as fraud before accepting the compromise proposal. UCO Bank took the commercial decision for accepting the compromise proposal for reducing any further loss to the Bank. There was specific mention in the complaint about two Bank officials viz. Shri C. Ramakrishna, the then Assistant General Manager and Shri A.K. Pattanaik, the then Senior Manager for accepting substitution of property without proper valuation and for observing that the substituted property was marketable. It was alleged that the appellants with the dishonest intention of causing wrongful loss to the Bank and corresponding wrongful gain to themselves fraudulently committed the act of cheating by substituting valuable properties offered as security with an encroached property and by siphoning of the Bank’s money; thus, committing the offence of cheating, criminal breach of trust, etc. under the IPC.

15.14. Upon registration of the FIR, CBI investigated the matter and thereafter submitted chargesheet before the Special Judicial Magistrate on 27.11.2018. As per the chargesheet, on the basis of forged copies of audit report appellants got enhancement of cash credit limit more than two times of the original amount. In the process, the UCO Bank was cheated resulting in wrongful loss of Rs. 223.74 lakhs with notional interest of Rs. 308.80 lakhs. Thus, appellant No. 1 had committed the offence of cheating and using of forged documents as genuine ones which are punishable under Sections 420 and 471 IPC. Insofar Bank officials are concerned, the chargesheet stated that investigation did not disclose any proactive role played by Bank officials in respect of sanction or renewal or enhancement of the cash credit limit; no criminal misconduct was found to have been committed by any of the Bank officials in this regard.

15.15. Vide order dated 20.02.2023, Special Judicial Magistrate framed charges against appellant No. 1 under Sections 420 and 471 IPC.

Analysis and reasoning

Cheating: What is meant by cheating? Explained

16. It can be seen from the above that charges have been framed only against appellant No. 1 under Sections 420 and 471 IPC. None of the Bank officials have been charge sheeted and, therefore, there is no prosecution under the PC Act. Substratum of Section 420 IPC is cheating and dishonest inducement leading to delivery of property. Cheating is defined under Section 415 IPC which says that whoever by deceiving any person, fraudulently or dishonestly induces the person so deceived to deliver any property to any person, etc. which causes or is likely to cause damage or harm to that person in body, mind, reputation or property, is said to ‘cheat’. Cheating is only one of the ingredients of Section 420, the other being dishonest inducement leading to delivery of property. ‘Dishonesty’ is defined in Section 24 IPC to mean deliberate intention to cause wrongful gain or wrongful loss to one person. When with such intention, deception is practiced and delivery of property is induced thereby then the offence under Section 420 of the IPC can be said to have been committed.

Section 417 IPC explained

16.1. Section 471 IPC on the other hand provides that whoever fraudulently or dishonestly uses as genuine any document or electronic record which he knows or has reason to believe to be a forged document or electronic record, shall be punished in the same manner as if he had forged such document or electronic record.

Judgments reference

16.2. This Court in Mohammed Ibrahim Vs. State of Bihar explained that to constitute an offence under Section 471 IPC, the requirement is that the document should be made or executed dishonestly or fraudulently with the intention of causing it to be believed that such document was made or executed by, or by the authority of a person, by whom or by whose authority he knows that it was not made or executed.

16.3. Again, in Deepak Gaba Vs. State of Uttar Pradesh, this Court examined the ingredients of Sections 420 and 471 IPC and observed that in order to apply Section 420 IPC viz. cheating and dishonestly inducing delivery of property, the ingredients of Section 415 IPC have to be satisfied. To constitute an offence of cheating under Section 415 IPC, a person should be induced, either fraudulently or dishonestly, to deliver any property to any person, or consent that any person, shall retain any property; the second class of acts set forth in the section is the intentional inducement of doing or omitting to do anything which the person deceived would not do or omit to do, if she were not so deceived. Thus, the sine qua non of Section 415 IPC is fraudulence, dishonesty or intentional inducement, and the absence of these elements would debase the offence of cheating. Referring to Mohammed Ibrahim, the Bench observed that for the offence under Section 420 IPC, there should not only be cheating but as a consequence of such cheating, the accused should also have dishonestly induced the person deceived to deliver any property to a person etc. Insofar as Section 471 IPC is concerned, the Bench again referred to Mohammed Ibrahim and observed that Section 471 IPC would be applicable when a person fraudulently or dishonestly uses as genuine any document or electronic record which he knows or has reasons to believe to be a forged document or electronic record. Unless the document is false and forged in terms of Section 464 IPC (making a false document) and 470 IPC (forged document or electronic record), the requirement of Section 471 IPC would not be met.

16.4. It may be mentioned that while Section 420 IPC is compoundable under Section 320 CrPC, Section 471 is not compoundable.

Question

17. The question is, whether, in a case of this nature, the offences under Sections 420 and 471 IPC can be said to have been made out against the appellants when the subject transaction was a banking one which ultimately led to a compromise settlement approved by the competent authority of the Bank and which had the imprimatur of the DRT. However, this issue need not detain us since we are focusing on the larger question of permissibility of continuance of criminal prosecution which was set in motion after settlement of the loan account on compromise between the borrower (appellants) and the Bank and which had the endorsement of the DRT.

Nikhil Merchant case

18. In Nikhil Merchant vs. Central Bureau of Investigation, CBI filed charges against the accused persons under Section 120B read with Sections 420, 467, 468 and 471 IPC read with Sections 5 (2) and 5 (1) (d) of the Prevention of Corruption Act, 1947 and Section 13 (2) read with Section 13 (1) (d) of the PC Act. One of the accused was the company whereas another one was Managing Director of the company. The other three accused were officials of Andhra Bank. Accused company had availed financial assistance from Andhra Bank but defaulted in repayment. Andhra Bank filed a suit for recovery and also lodged a complaint before the CBI which led to registration of FIR and filing of chargesheet in the Court of the Special Judge. The gist of the allegations against the accused persons was that they had conspired with each other in fraudulently diverting the funds of Andhra Bank; besides, offences alleging forgery were also included in the chargesheet.

19. The correctness of the view taken in Nikhil Merchant and two other cases was doubted by a subsequent coordinate Bench whereafter the matter was referred to a larger Bench. In Gian Singh Vs. State of Punjab4, the appellant was convicted under Sections 420 and 120B IPC. During pendency of the appeal against his conviction, appellant filed an application for compounding the offence. Thereafter, appellant also filed a petition under Section 482 CrPC for quashing of the FIR on the ground of compounding the offence. The petition under Section 482 CrPC was dismissed by the High Court.

3 Judge bench held Nikhil Merchant case was decided correctly

19.1. A three-Judge Bench of this Court considered the question as to whether the inherent power of the High Court to quash criminal proceedings against an offender who had settled his dispute with the victim of the crime but the crime is not compoundable under Section 320 CrPC should be invoked or not. After delineating the amplitude of the power under Section 482 CrPC and after discussing various case laws, the larger Bench held that the power of the High Court in quashing a criminal proceeding or FIR or complaint in exercise of its inherent jurisdiction under Section 482 CrPC is distinct and different from the power given to a criminal court for compounding the offence under Section 320 CrPC. Inherent power is of wide plenitude with no statutory limitation but it has to be exercised in accord with the guidelines engrafted in such power viz. (i) to secure the ends of justice or (ii) to prevent abuse of the process of any court. In what cases power to quash the criminal proceeding or complaint or FIR may be exercised where the offender and the victim have settled their dispute would depend on the facts and circumstances of each case and no category can be prescribed but before exercise of such power, the High Court must have due regard to the nature and gravity of the crime. Heinous and serious offences of mental depravity or offences like murder, rape, dacoity, etc. cannot be fittingly quashed even though the victim or victim’s family and the offender have settled the dispute. Similarly, any compromise between the victim and the offender in relation to offences under special statutes like the PC Act or offences committed by public servants while working in that capacity cannot provide for any basis for quashing criminal proceedings involving such offences. However, criminal cases having overwhelmingly and predominantly civil flavour stand on a different footing for the purposes of quashing, particularly the offences arising from commercial, financial, mercantile, civil, partnership or such like transactions or for that matter matrimonial disputes. In such category of cases, the High Court may quash the criminal proceedings if in its view because of the compromise between the offender and the victim, the possibility of conviction is remote and bleak and, therefore, continuation of the criminal case would put the accused to great oppression and prejudice and extreme injustice would be caused by not quashing the criminal case despite full and complete settlement and compromise with the victim. On that basis, the Bench held that Nikhil Merchant and the other two cases were correctly decided.

Compromise in Special Acts like P.C Act and Inherent powers

20. In Narinder Singh Vs. State of Punjab, the appellant faced charges amongst others under Section 307 of the IPC. A compromise was arrived at between the appellant and the complainant pursuant to which the appellant had moved the High Court under Section 482 CrPC for quashing of the FIR. High Court refused to do so on the ground that one of the four injuries suffered by the complainant was serious in nature as per medical opinion. This Court held that offences under Section 307 IPC would fall in the category of heinous and serious offences; therefore, such offences are to be generally treated as crime against the society and not against the individual alone. Such cases should not ordinarily be quashed. The Bench reiterated what was held in Gian Singh and held that those criminal cases having overwhelmingly and predominantly civil character, particularly those arising out of commercial transactions or arising out of matrimonial relationships or family disputes should be quashed when the parties have resolved their entire disputes amongst themselves. However, offences alleged to have been committed under special statutes like the PC Act should not be quashed merely on the basis of compromise between the victim and the offender. Finally, this Court held that while deciding whether to exercise its power under Section 482 CrPC, timing of settlement plays a crucial role. Those cases where settlement is arrived at immediately after the alleged commission of offence and the matter is still under investigation, the High Court may be liberal in accepting the settlement to quash the criminal proceedings.

21. Parbatbhai Aahir alias Parbatbhai Bhimsinhbhai Karmur Vs. State of Gujarat6 is a case where the High Court dismissed an application filed by the accused persons seeking quashing of FIR which was registered under Sections 384, 467, 468, 471, 120B and 506 (2) IPC. This Court after examining the precedents summarized and culled out the broad principles in the following manner:

“16.1 to 16.10”

21.1. Thus, this Court, while setting out the broad principles, held that the power to quash under Section 482 CrPC is separate and distinct from the power to compound under Section 320 CrPC and can be invoked even if the offence is non-compoundable.

22. This Court in Anil Bhavarlal Jain Vs. State of Maharashtra was examining an order passed by the High Court dismissing the petition filed by the appellants under Section 482 CrPC for quashing the FIR and the consequential chargesheet. In addition to IPC offences, the appellants were charged under Section 13(2) read with 13(1)(d) of the PC Act. In that case, some of the accused i.e. the appellants in the connected appeal were employees of the concerned Bank i.e. State Bank of India. The appellants had obtained a loan from the State Bank of India but failed to repay the same for which the loan account was declared as NPA. For recovery of the outstanding dues, State Bank of India approached the DRT where the matter was disposed of on consent terms. Thereafter, the Bank lodged a complaint before the CBI pursuant to which the FIR was registered whereafter chargesheets were filed. Appellants sought for quashing of the FIR and the chargesheet and filed a writ petition before the High Court under Section 482 CrPC. However, High Court dismissed the said writ petition observing that the appellant had a substantive alternative remedy under the provisions of the CrPC. Posing the question as to whether the criminal proceedings should be quashed based upon a settlement arrived at between the parties as per the consent terms drawn and submitted before the DRT, a two-Judge Bench of this Court observed that in view of the fact that a special statute i.e. the PC Act had been invoked, quashing of offences under the said Act would not be justified.

Bharthi Devi case:

23. In K. Bharthi Devi Vs. State of Telangana, the accused persons were granted various credit facilities by the Indian Bank which were secured by collateral security. As the accused persons failed to repay the dues, the loan account was declared as NPA and to realize the outstanding dues Indian Bank filed an original application before the DRT. During pendency of the proceedings before the DRT, Indian Bank lodged a written complaint before the CBI alleging that some of the title documents executed by the accused persons by virtue of which equitable mortgage was created were not original documents, rather those were fake, forged and fabricated. CBI registered an FIR whereafter chargesheet was filed stating that offences punishable under Sections 120B read with Section 420, 409, 467, 468 and 471 IPC and Sections 13 (1) (d) and 13 (2) of the PC Act were committed.

23.1. At that stage, the accused persons approached the Indian Bank for settlement. After negotiations, the parties arrived at a settlement whereafter the settlement amount was paid by the accused persons following which the Indian Bank issued no dues certificate to the borrowers (accused persons). DRT recorded that the dispute was settled in full satisfaction of the dues of the respondent-Indian Bank.

23.2. Thereafter, the accused persons filed a criminal petition before the High Court under Section 482 CrPC seeking quashing of the chargesheet. The High Court, however, rejected the said petition holding that the settlement arrived at was only a private settlement and was not a part of any decree given by any court. The charges include the use of fraudulent, fake and forged documents that were used to embezzle public money; if the charges were proved, those would be grave crimes against the society as a whole and hence merely due to a private settlement between the Bank and the accused, it cannot be said that prosecution of the accused persons would amount to abuse of the process of the court.

23.3. A two-Judge Bench of this Court referred to the previous decisions of this Court including Nikhil Merchant, Gian Singh, Narinder Singh, etc. and held that criminal cases having overwhelmingly and predominantly civil character, particularly those arising out of commercial transactions or arising out of matrimonial relationships or family disputes should be quashed when the parties have resolved their entire disputes among themselves. The Bench observed that the dispute involved in the said case had predominantly overtures of a civil dispute. After the settlement, the Bank had also closed the loan account. That apart, the Bench noted that in view of the settlement between the parties in a proceeding before the DRT, the possibility of conviction is remote and bleak. In such a case, continuation of the criminal proceedings would put the accused to great oppression and prejudice. Holding that it was a fit case where the High Court ought to have exercised its jurisdiction under Section 482 CrPC and ought to have quashed the criminal proceedings, the Bench allowed the appeal, set aside the order of the High Court and quashed the criminal proceedings.

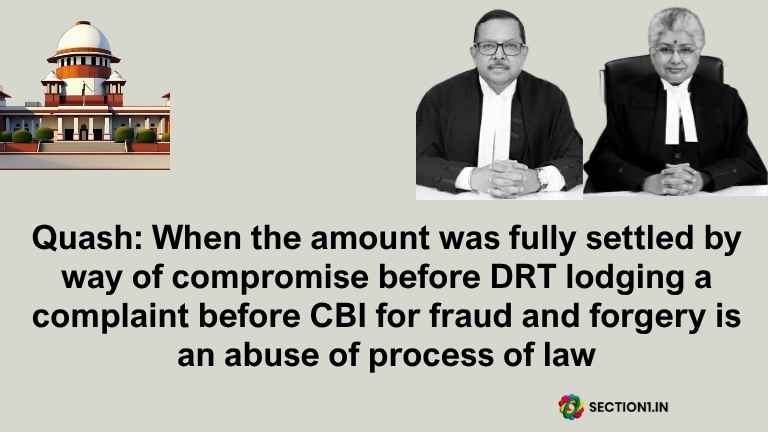

When the amount was fully settled by way of compromise before DRT lodging a complaint before CBI for fraud and forgery is an abuse of process of law

24. Applying the above principles to the facts of the present case, we find that in the pending proceedings before the DRT instituted by the second respondent-Bank, a negotiated compromise was arrived at between the parties. The settlement was approved by the competent authority of the respondent-Bank. Joint application was filed before the DRT by appellant No. 1 and respondent No. 2-Bank to place on record the settlement which was noted by the DRT and adjourned to a subsequent date to ensure compliance. Following the same, appellants paid the entire settlement amount whereafter the Bank issued no dues certificate to the appellants. Thereafter, on a further application by the respondent-Bank, the original application was dismissed as withdrawn by the DRT after noting that the claim to the outstanding dues were settled as per the compromise and the settlement amount was paid by the appellants whereafter no dues certificate was issued by the Bank. When the matter was fully settled which was endorsed by the DRT, the respondent-Bank after more than two years lodged complaint before the CBI to initiate criminal prosecution alleging fraud and forgery by the appellants. In the facts and circumstances, we are of the view that the present case is squarely covered by the decision of this Court in K. Bharthi Devi.

26. We are afraid, such conduct of the respondent Bank betrays lack of good faith. If the Bank had suspected fraud in 2013 itself, it should have lodged complaint at that stage itself. However, such stand of the Bank that fraud was committed by appellant No. 1 is not supported by the contents of the compromise settlement itself. We have already noted that in clause 9.1.9 of the compromise settlement, it was clearly mentioned by the Bank that there were no lapses in documentation or any irregularity was observed in the cash credit proposal of the appellants as per legal audit dated 12.02.2009. Additionally, the Bank certified in clause 25 that the compromise amount was in terms of the RBI policy guidelines and that it was not lower than the distress sale value of the securities available. After entering into a compromise settlement with the appellants wherein it was clearly stated that there was no tampering of any of the documents and after filing joint application before the DRT to record the compromise settlement, it was not proper on the part of the respondent-Bank to belatedly initiate criminal proceedings against the appellants, that too, after withdrawing the proceedings from the DRT on execution of the compromise settlement leading to closure of the loan account. Such a criminal proceeding in our view would not only be oppressive qua the appellants but would also amount to an abuse of the process of the court.

Reason for quash explained

28. There is one more reason why we say so. If the respondent-Bank is permitted to go ahead with the criminal prosecution initiated after settlement of the loan account before the DRT, it would adversely impact the sanctity of such settlement which has become part of the judicial proceeding and which had the approval of a judicial forum like the DRT. If such a conduct is overlooked and prosecution is allowed to continue, many persons including commercial entities would be hesitant to come forward and seek resolution of their disputes arising out of banking transactions which are after all commercial transactions, having predominantly elements of civil dispute(s). This in turn would have a debilitating effect on the overall economy, more so, when the focus is on settlement of commercial disputes. This is the larger picture we need to keep in mind.

Conclusion

29. For the aforementioned reasons, we allow this appeal and set aside the impugned order of the High Court dated 05.07.2024. Consequently, chargesheet dated 27.11.2018 and the charge framing order of the Special Judicial Magistrate dated 20.02.2023 are hereby quashed.

Resources

Judgments references

1. Mohammed Ibrahim Vs. State of Bihar

- Citation: (2009) 8 SCC 751

- Brief: Clarifies the essential ingredients required to constitute an offence under Section 471 of the IPC (using a forged document as genuine). The court noted that the document must be executed dishonestly or fraudulently with the specific intention of deceiving someone into believing it was made by an authority that did not actually authorize it.

2. Deepak Gaba Vs. State of Uttar Pradesh

- Citation: (2023) 3 SCC 423

- Brief: Examines the intersection of Sections 415, 420, and 471 of the IPC. It establishes that fraudulence, dishonesty, or intentional inducement are the sine qua non (essential conditions) for the offence of cheating, and that a charge under Section 471 fails unless the underlying document is proven to be false or forged under Sections 464 and 470 IPC.

3. Nikhil Merchant Vs. Central Bureau of Investigation

- Citation: (2008) 9 SCC 677

- Brief: A foundational case where the Supreme Court held that technicalities should not prevent the quashing of criminal proceedings (even those involving non-compoundable offenses like forgery) if the dispute has overwhelming civil or commercial overtones and has been fully settled via a compromise between the borrower and the bank.

4. Gian Singh Vs. State of Punjab

- Citation: (2012) 10 SCC 303

- Brief: A landmark three-judge bench judgment clarifying that the High Court’s inherent power to quash under Section 482 CrPC is distinct from a trial court’s power to compound under Section 320 CrPC. It ruled that while heinous or statutory crimes (like the PC Act) cannot be quashed, commercial, financial, or matrimonial disputes with a predominantly civil flavour can be quashed if a settlement renders the chance of conviction bleak.

5. Narinder Singh Vs. State of Punjab

- Citation: (2014) 6 SCC 466

- Brief: Reaffirmed the principles of Gian Singh, distinguishing serious crimes against society (like Section 307 IPC) from commercial or family transactions. It also emphasized that the timing of the settlement plays a crucial role in deciding whether the court should exercise its quashing powers.

6. Parbatbhai Aahir alias Parbatbhai Bhimsinhbhai Karmur Vs. State of Gujarat

- Citation: (2017) 9 SCC 641

- Brief: Summarizes and structures the broad legal principles governing the invocation of Section 482 CrPC based on settlements. It carves out a strict exception for economic offenses involving financial fraud or misdemeanors that hurt the State’s economic well-being, stating that such cases should not be easily quashed.

7. Anil Bhavarlal Jain Vs. State of Maharashtra

- Citation: 2024 SCC OnLine SC 3823

- Brief: Held that quashing a criminal case purely on the basis of consent terms drawn before the Debts Recovery Tribunal (DRT) is not justified if bank employees are charged under a special statute like the Prevention of Corruption Act (PC Act).

8. K. Bharthi Devi Vs. State of Telangana

- Citation: (2024) 10 SCC 384

- Brief: Dealt with a similar factual matrix where bank borrowers used allegedly fake title deeds to secure credit. The Supreme Court quashed the criminal case under Section 482 CrPC because a full settlement was later reached before the DRT, the loan account was closed, and the underlying nature of the dispute was overwhelmingly commercial and civil.

Acts and the Sections

Indian Penal Code, 1860 (IPC)

- Section 24: Definition of ‘Dishonesty’.

- Section 120B: Criminal conspiracy.

- Section 307: Attempt to murder.

- Section 409: Criminal breach of trust by a public servant, banker, etc..

- Section 415: Definition of ‘Cheating’.

- Section 420: Cheating and dishonestly inducing delivery of property.

- Section 464: Making a false document.

- Section 467: Forgery of valuable security, will, etc..

- Section 468: Forgery for purpose of cheating.

- Section 470: Forged document or electronic record.

- Section 471: Using as genuine a forged document or electronic record.

- Section 506(2): Criminal intimidation.

Code of Criminal Procedure, 1973 (CrPC)

- Section 320: Compounding of offences.

- Section 482: Saving of inherent powers of the High Court to quash proceedings.

Prevention of Corruption Act, 1988 & 1947 (PC Act)

- Section 13(1)(d) (1988 Act): Criminal misconduct by a public servant.

- Section 13(2) (1988 Act): Punishment for criminal misconduct.

- Section 5(1)(d) & 5(2) (1947 Act): Historical equivalents for criminal misconduct mentioned in cited case law.

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act)

- Section 13(2): Notice to borrower for enforcement of security interest.

Delhi Special Police Establishment Act, 1946

- Section 6: Consent of the State Government for the CBI to exercise powers and jurisdiction.

Party

Vijay Kumar Kela & Anr. versus Central Bureau of Investigation & Anr - Criminal Appeal No. 2974 of 2026 - 2026 INSC 588 - May 29, 2026 – Hon’ble Mr. Justice B.V. Nagarathna and Hon’ble Mr. Justice Ujjal Bhuyan.